A coordinated rebellion is quietly reshaping global finance – one that aims not just to escape dollar tyranny, but to bury it.

The Cradle

The era of the dollar's unchallenged global supremacy is fraying at the edges. What was once a cornerstone of global finance and trade is now a contested domain, as a growing number of states search for alternatives to the currency long used to enforce western diktats. The US dollar’s centrality to cross-border transactions and its role as the world’s reserve currency are no longer guaranteed – and this shift is no longer theoretical.

For decades, the dollar served as a universal medium of exchange, store of value, and unit of account. But these benefits came with steep costs. The system's dependence on a single state’s policies and its reliance on intermediary conversions generated layers of risk and friction. Today, those risks have become obstacles to the expansion of global trade. And as emerging economies gain confidence and weight, Washington is being forced to cede its monetary throne.

The dollar still reigns, but its grip is loosening

The dollar continues to dominate cross-border transactions, whether in current accounts or financial markets. It remains a trusted store of value for both institutional investors and individuals. But the tide is turning. Since the onset of the COVID-19 pandemic, central banks and private capital have steadily reduced their dollar holdings, redirecting value into gold and other tangible assets.

While the dollar is still used for standardizing global accounting, the utility of artificial intelligence (AI) and technological innovation now allows for currency baskets – like those composed of the BRICS nations (Brazil, Russia, India, China, and South Africa) – to easily substitute many of the dollar’s functions. In short, the era when no credible alternative existed is over.

BRICS and the rise of counterweight currencies

As the Global South expands its share in global trade and GDP, the practical use of non-dollar currencies is gaining traction. Within the BRICS bloc, transactions are increasingly being conducted in national currencies.

SWIFT (Society for Worldwide Interbank Financial Telecommunication)—the western-dominated messaging network used by banks for cross-border payments—remains dominant, but alternatives are gaining ground. Data shows that by May 2025, China’s yuan, which accounted for just 2 percent of global payments, already facilitated 50 percent of BRICS-internal trade.

While the BRICS payment system is still far from global acceptance, its presence is growing. And behind this momentum lies a strategic understanding: true monetary sovereignty cannot coexist with dependency on hostile financial systems.

CBDCs: A digital leap toward multipolar finance

The greatest barrier to building multipolar alternatives is not political will but infrastructure. Replacing SWIFT requires secure, scalable, and interoperable platforms. Here, central bank digital currencies (CBDC) – blockchain-based digital versions of national currencies issued and regulated by central banks – offer a transformative pathway. Unlike cryptocurrencies, CBDCs are fully backed and controlled by sovereign monetary authorities, combining digital speed with state oversight.

Beijing is leading the charge. The People’s Bank of China has expanded its Cross-Border Interbank Payment System (CIPS), an alternative to SWIFT designed for yuan transactions and increasingly integrated with CBDC platforms.

According to its estimates, CBDCs can reduce transaction costs by up to 50 percent and clear cross-border payments in seconds. SWIFT, by contrast, depends on a slow, layered correspondent banking model that can take days and imposes heavy fees.

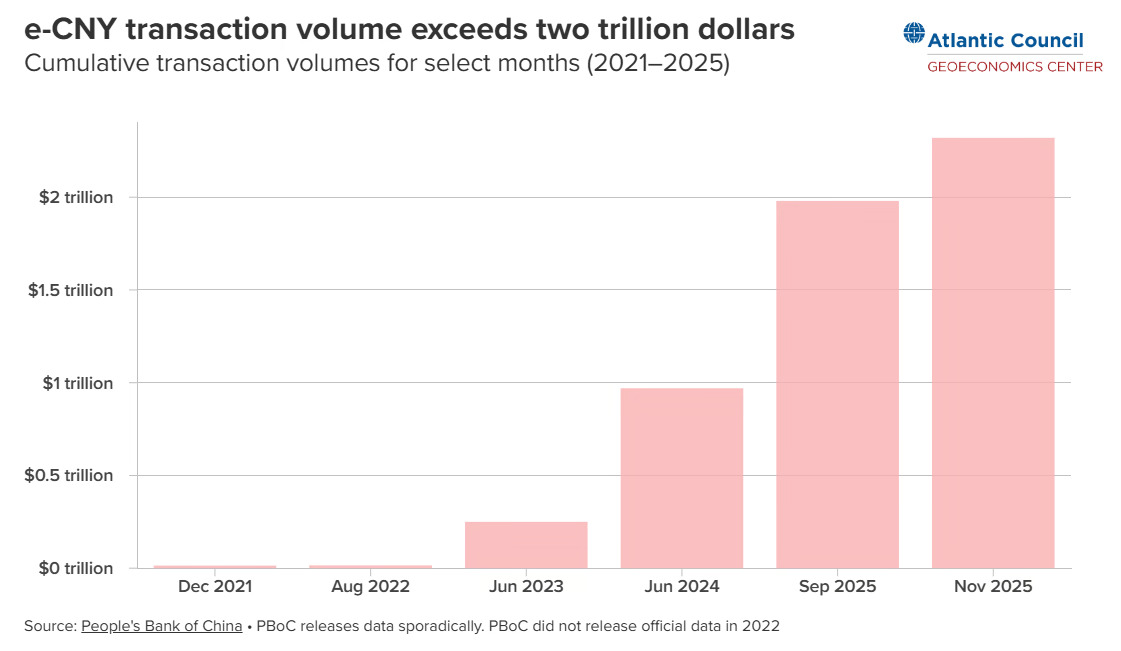

Digital yuan surges past $2 trillion

This is why China’s digital yuan (e-CNY) has grown by over 800 percent since 2023, exceeding $2.3 trillion in transaction volume by the end of 2025. To increase domestic adoption, China is employing a strategy that preserves the sovereignty and regulation of e-CNY while incorporating interest-bearing features and stablecoin-like functionality.

Project mBridge – short for “multiple CBDC Bridge” – is a joint initiative developed by the Bank for International Settlements Innovation Hub and the central banks of China, Hong Kong, Thailand, and the UAE. It enables real-time, cross-border payments using CBDCs on a shared blockchain platform without the need for correspondent banks or SWIFT messaging.

In 2025, mBridge processed $55.49 billion in transactions – a 2,500-fold increase from early 2022 trials. Over 95 percent of its volume is in e-CNY, challenging early forecasts that CBDCs, and especially China’s, would suffer from public skepticism and limited use cases.

Five years after its launch, e-CNY remains the world’s largest central bank digital currency experiment. And its success is reshaping assumptions about who can set the pace in financial innovation.

West Asia's fintech frontlines

The shift is not confined to East and South Asia. In West Asia, the UAE is taking the lead in digital payments. A new platform backed by China and tested by the central banks of the UAE, Saudi Arabia, Hong Kong, and Thailand has already executed more than 4,000 cross-border transactions. The UAE’s Ministry of Finance recently completed the first state transaction using wholesale digital dirhams.

Beijing’s designation of First Abu Dhabi Bank as its second yuan-clearing institution in the Emirates marks a deeper step in regional monetary integration. Unlike previous appointments of Chinese institutions abroad, this move elevates a local bank, signaling both strategic trust and intent to build regional nodes of financial autonomy.

This builds on earlier shifts, including the landmark 2023 deal in which the UAE and China settled a liquefied natural gas (LNG) trade in yuan – the first of its kind and a symbolic rupture from the petrodollar system.

BUNA and the architecture of monetary autonomy

The Arab Regional Payment Clearing and Settlement Organization, known as BUNA, is another critical piece of the emerging payment architecture. Headquartered in the UAE and operated by the Arab Monetary Fund, BUNA is a cross-border and multi-currency payment platform created to facilitate trade and investment flows within and beyond the Arab world.

It enables central and commercial banks to send and receive payments in multiple currencies across the Arab region and with global partners. Monthly transaction volumes have grown into the thousands, and BUNA continues to expand participation. While its long-term strategy includes interoperability with other regional and global systems, such as India’s UPI or China's CIPS, no fixed timeline or confirmed list of new currencies has been officially announced.

Ren Haiping, Deputy Head of Strategic Research at the China Center for International Economic Exchanges, has noted that expanding BUNA’s currency reach – including adding the rupee and yuan – could improve financial market infrastructure and deepen cooperative economic ties, including cross‑border trade and investment linkages between participants.

This is echoed by broader Gulf initiatives like AFAQ, the Gulf Instant Payment System launched by the Gulf Cooperation Council (GCC), which connects member-state banks and facilitates real-time cross-border transactions without relying on dollar-clearing banks. AFAQ is designed to create a unified regional payment ecosystem that offers fast, secure, and efficient settlement of transactions within the Arab states of the Persian Gulf.

No monetary revolution without institutional transformation

Despite China’s digital advances, no single state can anchor a new global system alone. The transformation will require institutional architecture – a clearinghouse like the postwar European Payment Union (EPU), which helped stabilize intra-European trade by settling imbalances multilaterally rather than bilaterally in scarce US dollars.

The New Development Bank (NDB) within BRICS is best positioned to lead this. But entrenched global power dynamics – not just financial inertia – remain the real obstacle. Under the US government of President Donald Trump, Washington escalated both economic and military pressure to stifle such shifts. Its weaponization of sanctions in Venezuela and Iran was a clear warning.

Trump openly frames dollar dominance as a matter of national security, and even a legitimate ‘casus belli.’ This mindset persists in both US political parties and has become a cornerstone of Atlanticist policy.

Dollar still dominates finance – but the cracks are widening

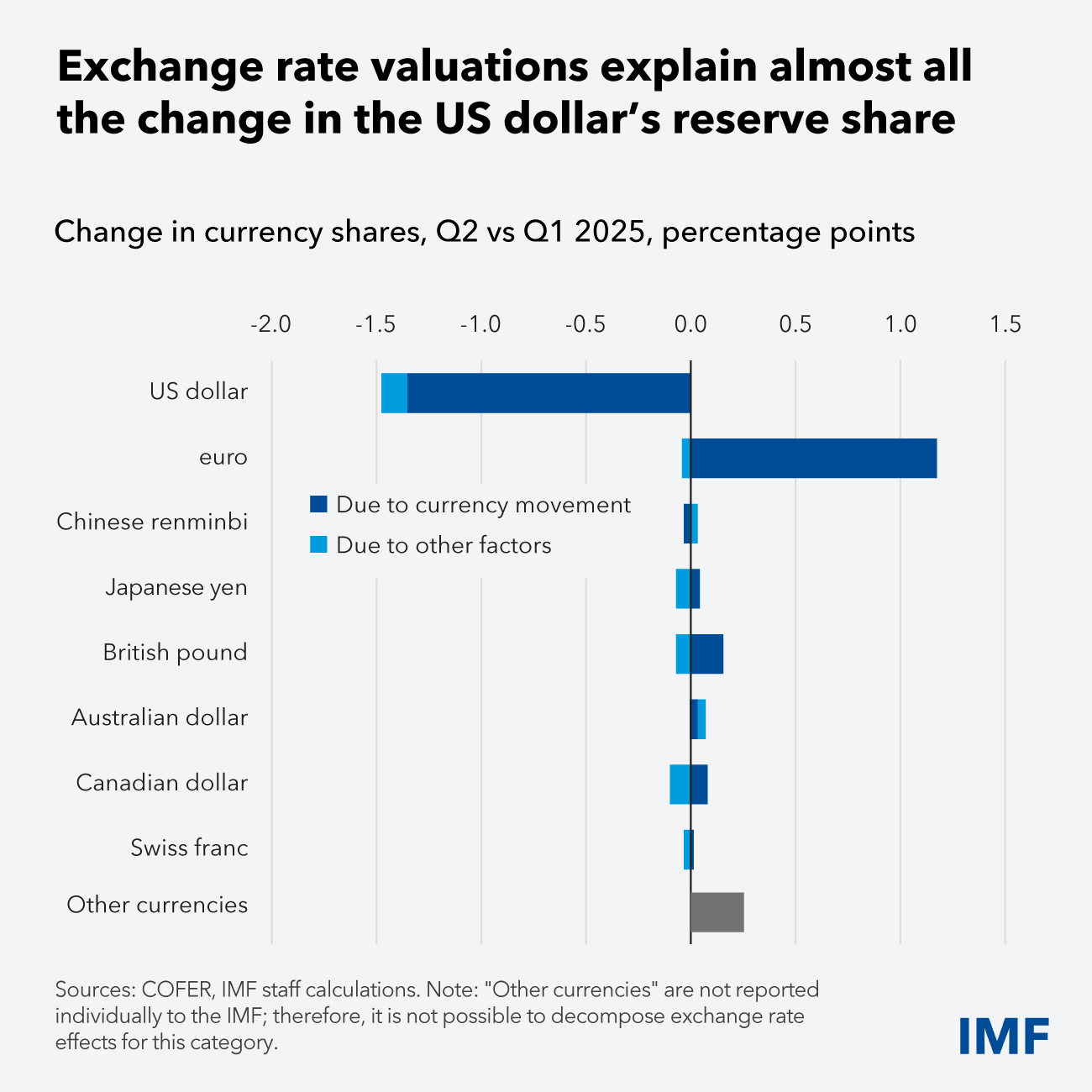

Despite losing ground in trade, the dollar still dominates cross-border finance. In 2024, global goods and services trade reached $33 trillion – about a third of global GDP. Yet according to the Bank for International Settlements, daily FX turnover stood at $7.5 trillion – more than five times the annual trade volume. That market remains overwhelmingly dollar-based.

In 2022, the dollar featured in 88 percent of all FX transactions. By April 2025, its share had even risen slightly to 89.2 percent. The euro declined to 28.9 percent (from 30.6 percent in 2022). The yen remained stable at 16.8 percent. Meanwhile, the yuan rose to 8.5 percent – a steady climb since 2013. Yet much of the dollar’s dominance now comes not from strength, but from weakness elsewhere: the euro and pound’s decline has only reinforced its position.

From bypassing SWIFT to building the future

China knows it cannot dismantle dollar dominance alone. BRICS and the broader Global South must lead the charge. The architecture is already taking shape. By January 2025, countries including Russia, Iran, Venezuela, Saudi Arabia, China, the UAE, and Egypt had begun using the “petro-yuan” in cross-border energy transactions.

For Moscow, this shift is a direct response to sanctions and an effort to escape the grip of SWIFT and dollar-based trade. The move has worked – not symbolically, but materially. And as others follow, what was once a bypass strategy is becoming the nucleus of a new system.

An opening for the multipolar moment

The Greenland conflict is opening new opportunities for the Global South, as US geopolitical pressure and financial market risks may push Europe to reduce dollar dependence and move away from US assets. Investors may shift toward safe havens like the Swiss franc or strengthen economic ties with Beijing. These dynamics could accelerate the development of alternative payment systems.

This evolving crisis of dollar supremacy has exposed a deeper political rupture beneath the surface of shifting financial balances. The Global South is no longer willing to fund, facilitate, or remain vulnerable to an imperial system that serves its own economic subjugation.

New institutions are being born, old systems are fraying, and the illusions of inevitability that once upheld US financial primacy are shattering. The monetary order that emerges next will not be dictated from Washington, but forged in the shared interest of those long excluded from its spoils.

No comments:

Post a Comment