The Cradle

The pipeline project is not merely about energy. Although Europeans initially sought solace in the notion that Russia had lost its customers by cutting itself off from their energy markets, they in fact triggered Moscow’s strategic redirection of its energy toward the east. PoS-2’s strategic weight lies in its capacity to rewire Eurasian trade routes, provide Beijing with a reliable alternative to US-aligned LNG exporters, and consolidate a new axis of economic resilience outside the western-controlled system.

As Moscow seeks to offset the collapse of its European gas market, and China shores up long-term energy security, PoS-2 marks a turning point in the global energy order, away from US dominance and toward a multipolar, Eurasia-led future.

From exclusion to integration

The signing ceremony between the Russian Federation and the People’s Republic of China took place after the Shanghai Cooperation Organization (SCO) summit in Tianjin. It also coincided with the 80th anniversary of China’s liberation from Japanese occupation, marked by a military parade of the People’s Liberation Army.

PoS-2 sends a powerful message, both to the west and the Global South: Unipolarity is obsolete. The era of coercive Atlanticist dominance is over. With the rise of the SCO, BRICS, and deepening military and economic alliances across Eurasia, it is fair to say that multipolarity is no longer mere rhetoric.

PoS-2 is the result of years of Gazprom planning. Although Moscow delayed its development since the early 2020s, primarily due to price disputes, route alterations, construction costs, and scheduling concerns, these hurdles were eventually overcome, just as they were with PoS-1. That pipeline now transports 38 bcm annually to China, valued at $400 billion, and is set to rise to 44 bcm per year. Supplies through the Far Eastern route and Sakhalin Island, through a proposed new connector to PoS-1, are scheduled to begin in 2027 and are expected to grow from 10 bcm to 12 bcm per year. PoS-1 and PoS-2 both emerged under similar geopolitical conditions. After Crimea’s annexation in 2014 and under western sanctions, Moscow turned eastward as China invested in the Yamal LNG project in Siberia, worth $27 billion. Together, CNPC and the Silk Road Fund hold around 30 percent equity share alongside Novatek (50.1 percent) and Total.

A route through resistance

As Gazprom sought to maximize Yamal gas exports to Europe through Nord Stream 1 and 2, it also launched the Eastern Gas Development Program in 2007 – targeting the Chinese market with integrated supply systems connecting East Siberia (PoS-1) and Southeast Asia (PoS-3). PoS-2 was long suspended, but now demands rapid acceleration.

Mongolia’s Prime Minister Luvsannamsrai told the Financial Times in July 2022 that the feasibility study for PoS-2 had been completed and that construction was expected to begin in 2024. While an earlier proposal envisioned a route through the Altai Mountains into China’s Xinjiang region, by 2019, Beijing had signaled a preference for a path from Irkutsk through Mongolia into the Chinese capital. Environmental concerns from Altai’s local authorities also influenced this decision. The route is now largely set, with only minor modifications anticipated.

China, the world’s biggest gas buyer

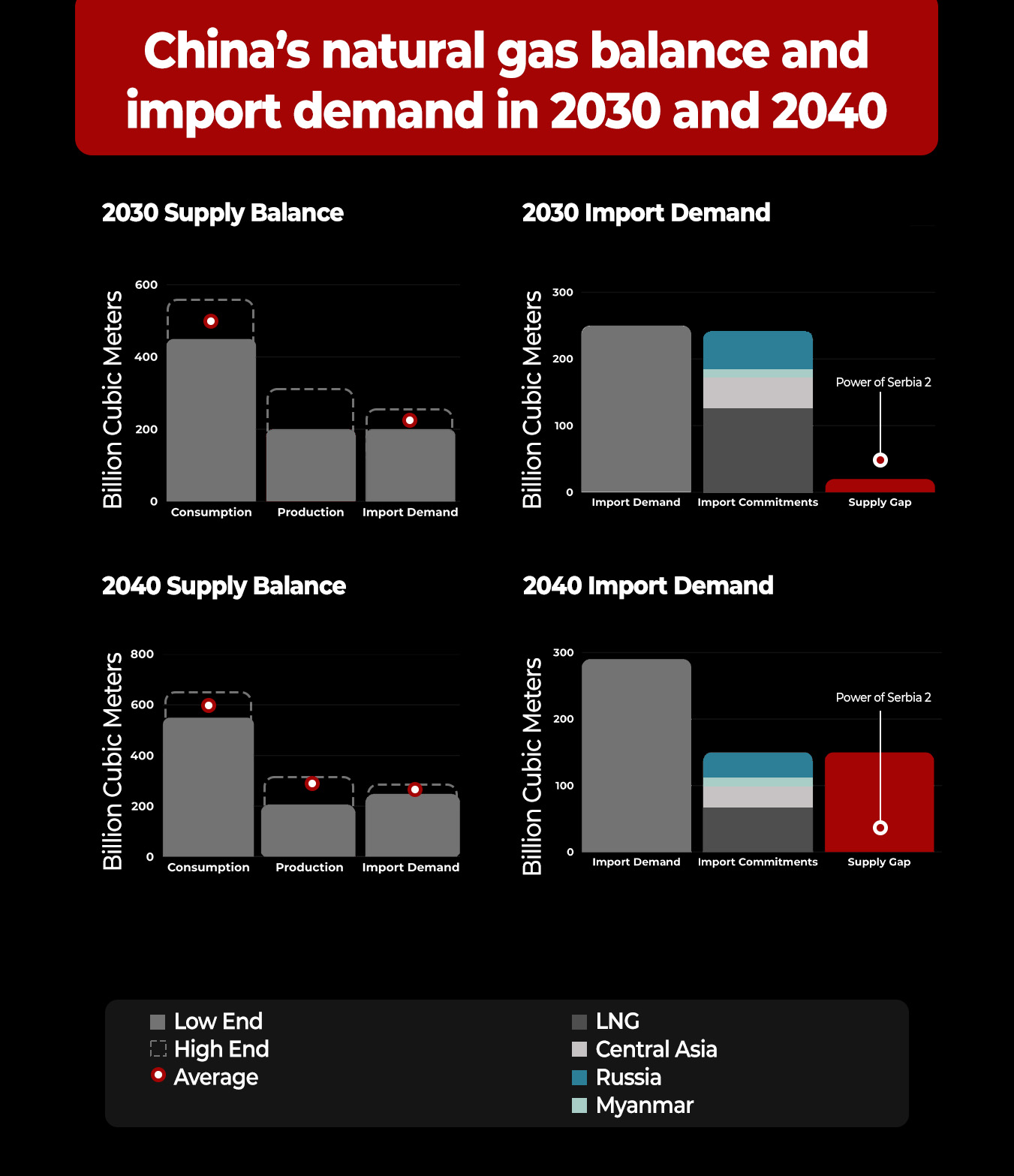

China leads the world in gas imports, both via pipeline and sea. Since 2021, it has topped global LNG imports. In 2024 alone, it imported 107 bcm of LNG and 71 bcm via pipelines.

International Energy Agency (IEA) data show that China’s LNG imports have been falling (year-on-year) amidst weak demand and rising competition with Europe for LNG cargoes. At the same time, China is expanding its pipeline gas import capacity, a shift that analysts say could gradually reduce China’s dependence on LNG.

Currently, gas flows from Turkmenistan (35 bcm), Myanmar (12 bcm), and Russia via PoS-1 (38 bcm) are key. Moscow and Beijing have also agreed to increase PoS-1 flows to 44 bcm annually. China’s strengthened position secures supply while enhancing bargaining power, a lesson not lost on US allies like Australia, which was recently forced to lower LNG prices in its long-term contract with Sinopec.

Cracks in the western order

Since 2018, Beijing has prioritized boosting domestic gas exploration and production – successfully raising output from 190 bcm in 2020 to 230 bcm by 2024. China’s energy mix is shaped by supply security, geopolitical factors, costs, and environmental priorities, balancing gas, LNG, crude, coal (domestic and imported), nuclear, and renewables. This shift could weaken the market position of traditional exporters like the US, Canada, Australia, and Qatar – especially in Southeast Asia and European spot markets.

Qatar, one of China’s top LNG suppliers, still faces uncertainty despite signing several major long-term contracts with Chinese firms in 2023, including 27-year supply deals with CNPC and Sinopec. While these agreements provide some stability, Doha’s overall position in the Chinese market remains less secure compared to Russia’s expanding pipeline commitments. Chinese energy companies continue to weigh Qatar’s reliability after Israel’s recent act of aggression, US bases on its soil, and the potential closure of the Strait of Hormuz.

Qatar may be forced to offer deeply discounted prices to remain competitive. It could ramp up production to drive prices down or limit volumes to maintain high prices – but only for a while.

Dollar dethroned?

There’s no doubt that PoS-2 will transform the global gas market. LNG trade will suffer, and the impact will extend to maritime shipping. Some large tankers may be rendered obsolete.

By 2030, as China reduces LNG imports, other importers will gain leverage. Some LNG projects may collapse altogether. Exporters like the US and Qatar are already uneasy. Washington is especially alarmed by the potential decline of dollar-based energy trade – a far more damaging blow than losing the Chinese LNG market. Gazprom’s CEO Miller says PoS-2 payments may be split evenly between the yuan and the ruble. This directly challenges the dollar’s energy dominance. Iraq’s late Saddam Hussein faced the wrath of Washington for daring to price oil in euros. But Russia and China are not Iraq.

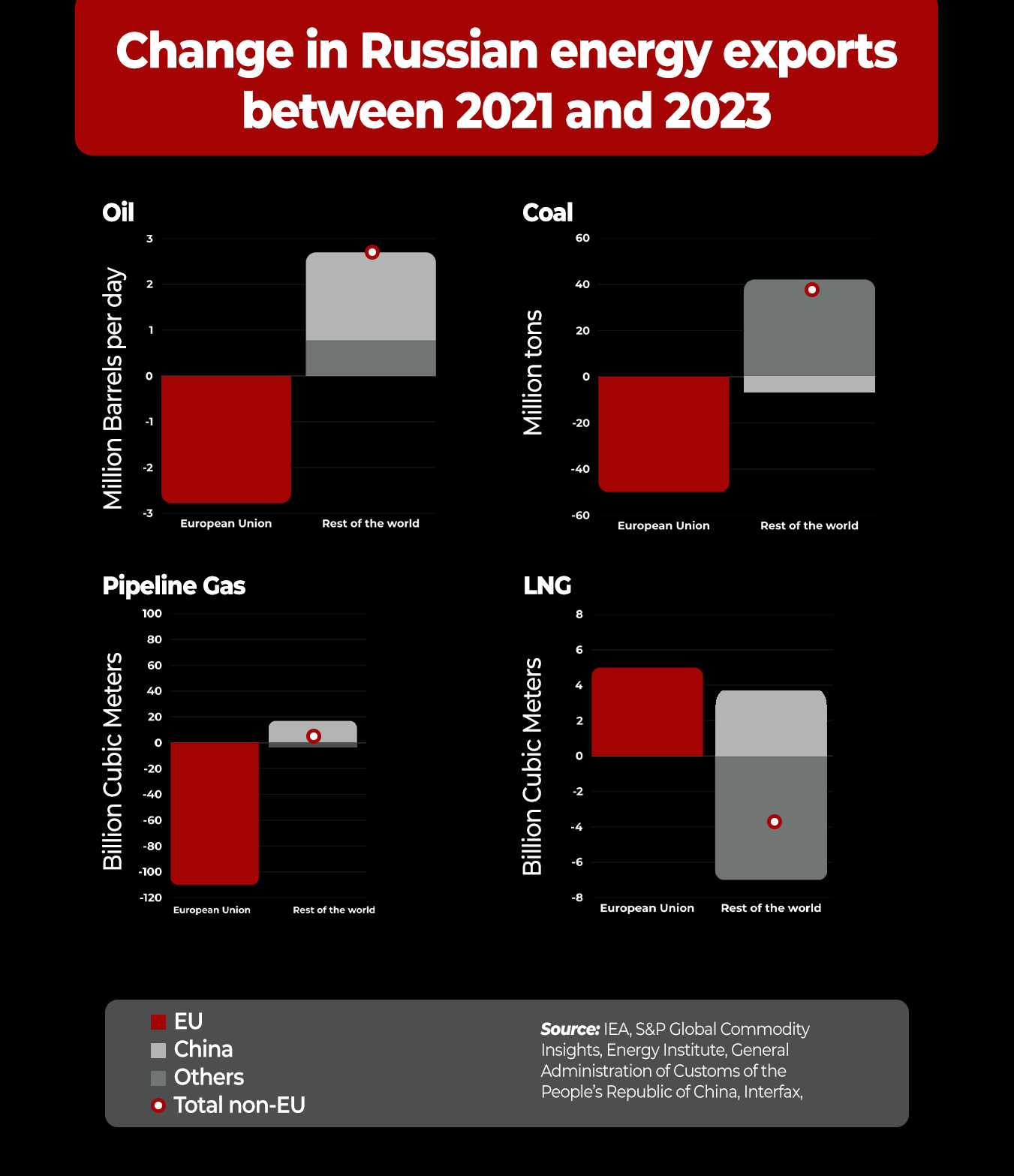

Some argue that China is becoming too dependent on Russian energy. But the dependency is mutual. In an era where both states face aggressive containment by the US and its partners, such interdependence is strategic, not risky. Moscow, moreover, is shedding unreliable European customers. In 2021, 80 percent of Russian pipeline gas and 40 percent of LNG exports went to Europe, about 150 bcm in total. That market is nearly lost. But PoS-2 can recover much of that revenue while anchoring Russia in the Asia-Pacific energy orbit.

More than profit

PoS-2 may be less profitable than its predecessor due to higher construction costs and lower prices. But tax breaks could help. More importantly, the project will create domestic contracts, boost steel production, and drive development in eastern Russia, a key Kremlin objective. Gazprom, which posted a $6.8-billion net loss in 2023 – its first since 1999 – and a $13.1-billion net loss in 2024, has no other major infrastructure project apart from PoS-2 and the suspended Baltic LNG terminal. For Gazprom, it is existential.

One reason China did not rush into the deal is that it may not need extra gas until the mid-2030s. Imports, currently around 150 bcm, are expected to rise to 250 bcm by 2030 – mostly covered by existing contracts. But projections suggest there will be room for PoS-2 by 2035. PoS-2 will also accelerate China’s rise as a global LNG player. An additional 50 bcm in pipeline gas will help Chinese firms optimize imports, boost re-export capabilities, forge joint LNG strategies, and expand regasification infrastructure abroad.

Wider PoS-2 adoption, long-term LNG contracts, and expanded global trade will position China as a global LNG stabilizer by the 2030s, with far-reaching implications for energy geopolitics. Viewed from any angle, PoS-2 is a win for multipolarity. It bypasses western attempts at containment, offers a development model for the Global South, and accelerates BRICS expansion. Most critically, it chips away at the dollar’s long-standing energy dominance. That may prove to be the pipeline’s most enduring impact, and the west’s greatest loss.

No comments:

Post a Comment