The blockade at Hormuz has throttled global energy flows, driving price shocks and exposing deep fractures from the Persian Gulf to Europe and Asia.

Suleyman Karan

The Cradle

.jpeg)

The issue extends beyond broken supply chains. Price escalation across crude and petrochemical markets has already begun to ripple outward.

Since the US-Israeli war on Iran that started on 28 February, crude prices have surged from roughly $70 per barrel to around $120 by the end of April, with refined products rising even faster amid tightening supply and logistical strain.

Fuel markets under strain

The closure of Hormuz has forced export-oriented refineries to scale back operations or halt production entirely as storage capacity fills. More than 4 million bpd of refining capacity is now at risk. While production elsewhere can theoretically compensate, transport and supply constraints limit how far that adjustment can go.

The most immediate pressure has emerged in diesel and jet fuel. What began as warnings from the International Energy Agency (IAE) has materialized into concrete disruptions. The German airline Lufthansa has already announced the cancellation of 20,000 flights due to fuel shortages, while the Dutch airline Transavia has followed with cuts to its schedule through May and June. IATA data shows jet fuel prices in Europe have risen by over 105 percent year-on-year.

Declining supplies of liquefied petroleum gas (LPG) and naphtha have forced petrochemical producers to scale back polymer output, compounding losses across the sector. Consumer countries have leaned on existing reserves to soften the blow. Global stockpiles of crude and refined products stand at around 8.2 billion barrels, roughly half held by Organisation for Economic Co-operation and Development (OECD) states.

IEA members agreed in March to release 400 million barrels from emergency reserves, but such measures can only delay deeper disruptions. They do not resolve the structural damage unfolding across production and distribution networks.

Structural damage and limited relief

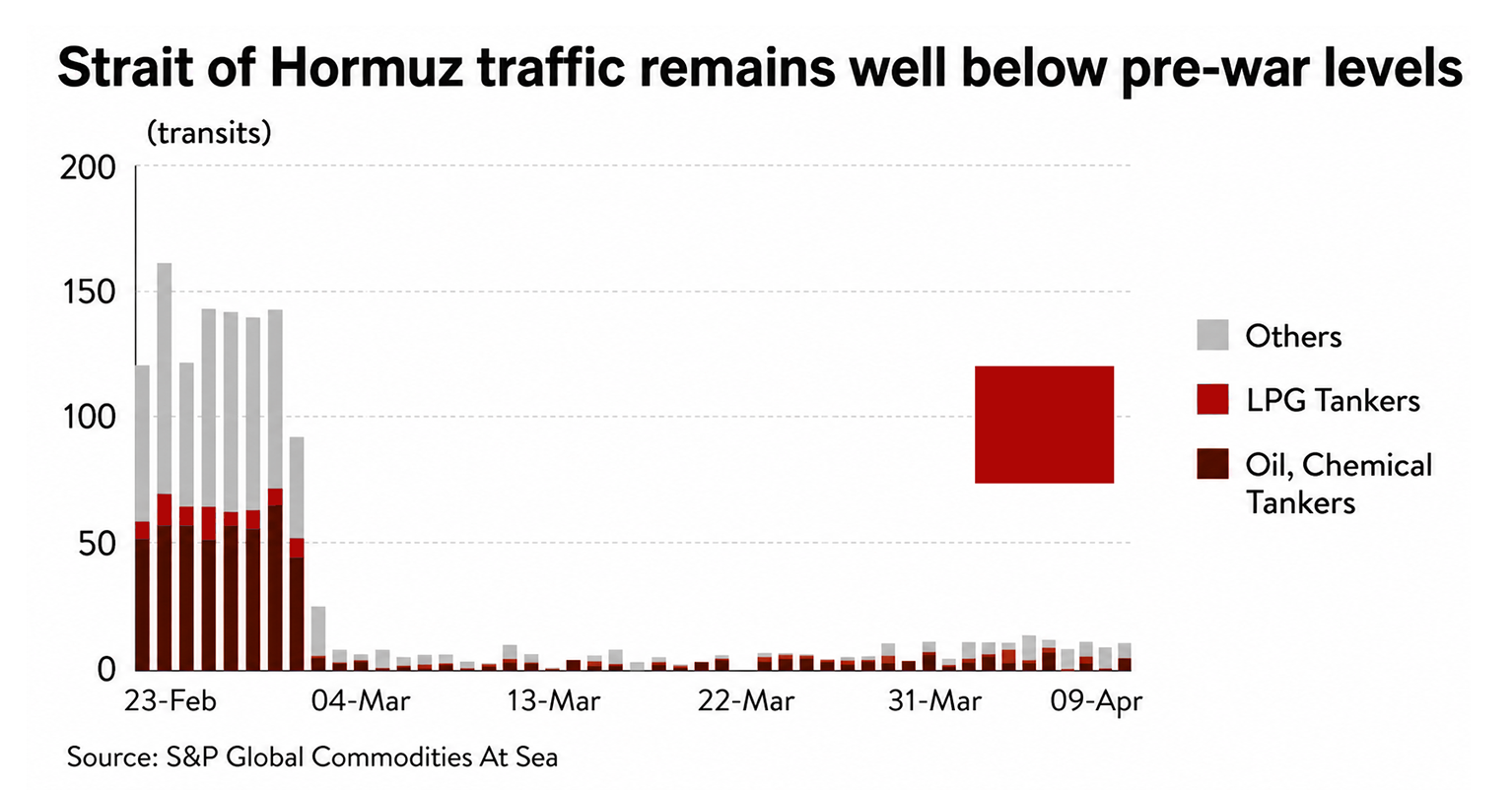

The scale of damage to energy infrastructure across the Persian Gulf is significant. Fatih Birol, executive director of the IAE, has warned that energy output lost in the conflict could take around two years to recover. Shipments tied to pre-war contracts continue, but new tanker loadings stalled in March, cutting off flows to Asia.

Oil-producing states along the Gulf are absorbing the heaviest impact. Facilities have been hit, output reduced, and losses mount with each passing day. A full damage assessment remains out of reach, though projections suggest recovery will take several years.

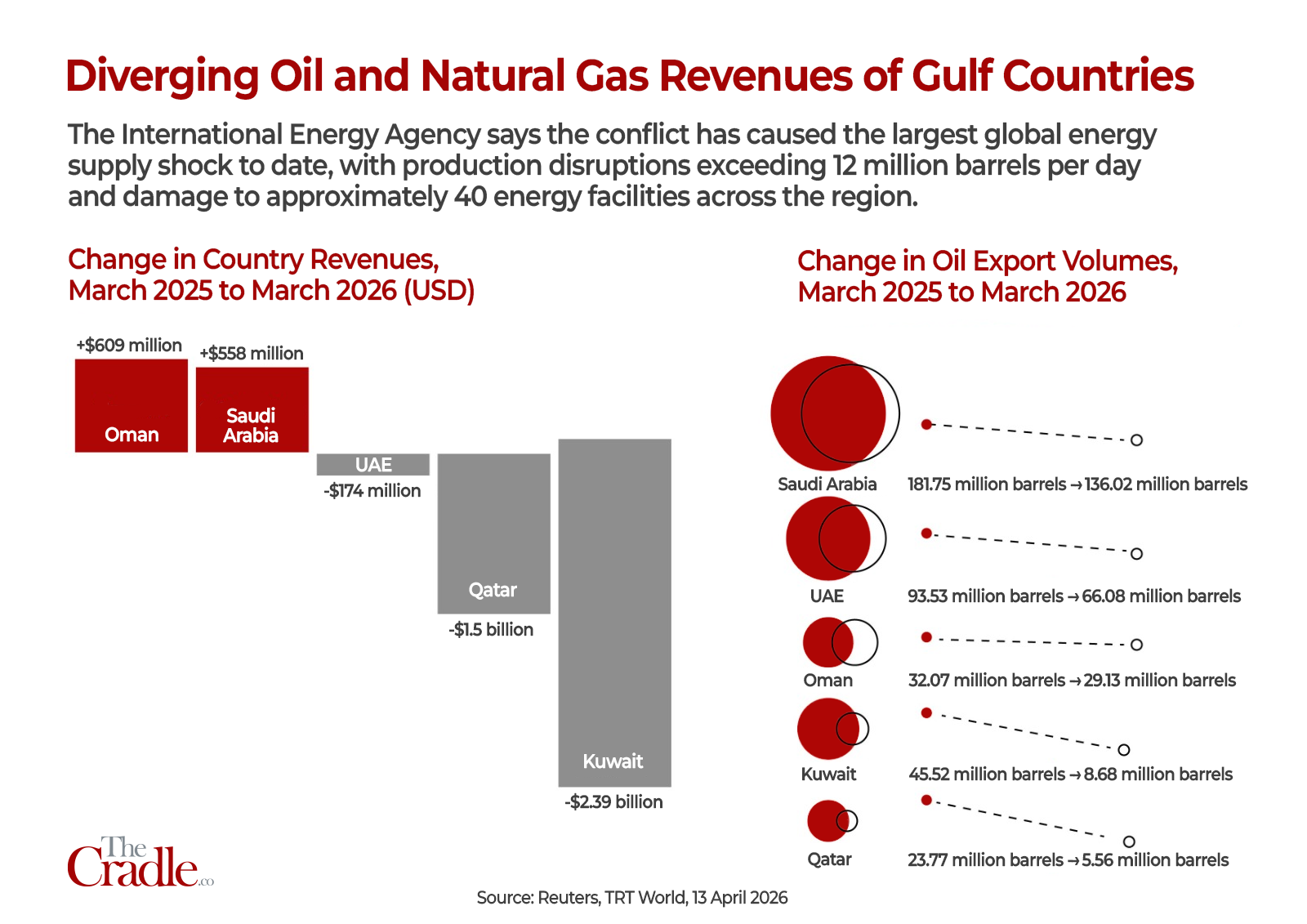

Saudi Arabia’s production capacity has suffered measurable damage. Qatar has lost close to one-fifth of its liquefied natural gas (LNG) output, a gap that will not be quickly repaired. Across the region, an estimated 2.4 million bpd of refining capacity is offline. Around 10 percent of global crude production remains disrupted, a deficit that cannot be offset while Hormuz stays closed.

Even under favorable conditions, a ceasefire and reopening of the strait would not bring immediate normalization. Markets would require at least six months to stabilize.

Constrained alternatives

Saudi Arabia has also confirmed a reduction of 600,000 bpd in production capacity and a 700,000 barrel decline in flows through its East–West Pipeline. This route, linking Gulf fields to the Red Sea, has been central to maintaining exports. Damage to a pumping station shortly after the ceasefire announcement underscored its vulnerability.

Additional strikes on the Manifa and Hurays fields have cut output by around 300,000 bpd. Overall, Saudi production capacity has fallen by at least five percent. Even if Hormuz reopens, the kingdom will struggle to fully compensate for lost volumes.

Qatar’s position as a key LNG supplier has also been compromised. Following strikes linked to the wider conflict, the Ras Laffan industrial complex sustained damage that will take years to repair. QatarEnergy estimates that around 17 percent of LNG export capacity has been affected, with restoration timelines ranging from three to five years.

The impact extends further. A gas-to-liquids facility operated jointly with Shell has also been hit, reducing capacity for at least a year. Annual losses of around 12.8 million tonnes of LNG are now expected.

Fractures within OPEC and regional fallout

The UAE’s decision to leave OPEC marks a significant shift within the energy bloc. Economic pressures and political tensions both appear to have shaped the move. Long-standing dissatisfaction with production quotas has converged with the economic strain imposed by the war.

The departure is likely to deepen friction with Saudi Arabia while raising broader questions about the cohesion of OPEC itself. It would not be an exaggeration to say that Dubai did not take this decision alone. It should be viewed as a new phase in plans by Washington and Tel Aviv to create a rupture in the Gulf and weaken OPEC’s cartel status. With the decision coming into effect today, the UAE ends its 58-year membership in the cartel.

The conflict has also exposed vulnerabilities within the UAE’s own energy infrastructure. The Ruwais Refinery, with a capacity of 922,000 bpd, was among the earliest targets. Gas processing operations at Habshan were suspended multiple times, while explosions at offshore fields halted production.

Fujairah Port has allowed exports to continue outside Hormuz, but repeated attacks on storage and transport facilities have forced intermittent shutdowns. The extent of disruption would have been far greater without this alternative route.

A region’s energy lifelines under pressure

A region’s energy lifelines under pressureKuwait’s Mina al-Ahmadi and Mina Abdullah refineries have sustained repeated strikes but remain operational. Before the war, both were significant suppliers of jet fuel to Europe and refined products to Asia. Disruptions to these flows have intensified supply concerns across both regions.

Iraq, OPEC’s second-largest oil producer, has been among the hardest hit due to its lack of alternative export routes. The effective closure of the strait forced the country to halt more than three-quarters of its production, reducing output from 4.3 million bpd to around 800,000.

Attacks on infrastructure, including the Rumaila field, have compounded the crisis. Iraq’s internal divisions further complicate the picture, with competing actors backed by regional powers. Even if the current conflict subsides, the country remains exposed to renewed instability.

Iran has absorbed multiple strikes targeting fuel depots and energy facilities, including attacks on the South Pars Gas Field. While key export infrastructure at Kharg Island has largely avoided damage, several production units have been taken offline.

Despite economic pressure, the war has produced a degree of internal consolidation. The more difficult phase may come after hostilities end, when the country must attempt to stabilize both its economy and energy sector.

Oman has faced comparatively limited disruption and may emerge in a more stable position than its neighbors. Operations at Salalah Port have been affected, prompting Maersk to suspend activity, but the scale of damage remains contained.

Bahrain presents a different case, having declared force majeure on 9 March following an attack on the Sitra Refinery, effectively shutting operations. Damage is severe, and full recovery could take months. More pressing for Bahrain is domestic unrest, with tensions between the Sunni ruling minority and Shia majority raising fears of renewed uprising.

Global spillover and shifting balances

The impact of the conflict extends well beyond the Gulf. South Asia’s emerging economies and Japan have borne some of the highest costs, as anticipated. China appears better positioned, benefiting in part from its preparedness and the relative weakening of regional competitors.

Tensions in the Strait of Malacca add another layer of uncertainty, raising the possibility of further disruptions to global trade routes.

Europe is also set to absorb a significant share of the burden. Energy costs have already surged since the Russia–Ukraine war, and the current crisis affects both supply shortages and price pressures.

By contrast, energy-rich economies in the Americas are better insulated, while import-dependent states face mounting strain. Africa reflects a similar divide, with producers such as Algeria and Nigeria positioned to benefit, while others remain vulnerable.

Long-term uncertainty

The damage triggered by the Hormuz crisis will take at least two years to address, and likely longer. Global growth forecasts for 2026 are already being revised downward.

Even under relatively stable conditions, the economic cost will weigh heavily on Gulf producers, as well as on Asian and European economies. Slower growth in East and South Asia in particular carries wider implications for global demand.

Crude prices are unlikely to return to pre-war levels near $70 in the near future. Transport, insurance, and freight costs will remain elevated, feeding into broader commodity inflation. Fragilities within the global financial system are expected to deepen as a result.

As a new balance begins to take shape, further tensions appear likely. The longer-term consequences may extend beyond energy markets, intersecting with climate pressures that continue to intensify in the background.

No comments:

Post a Comment